The Inflation We Warned About Has Arrived

8 May 2026

Six weeks ago as Chief Economist at Payble we ran an emergency webinar for council leaders on the state of the Australian economy. Last week's CPI data validated almost every thread of that argument and the most concerning chapter hasn't been written yet.

What the March 2026 CPI release showed

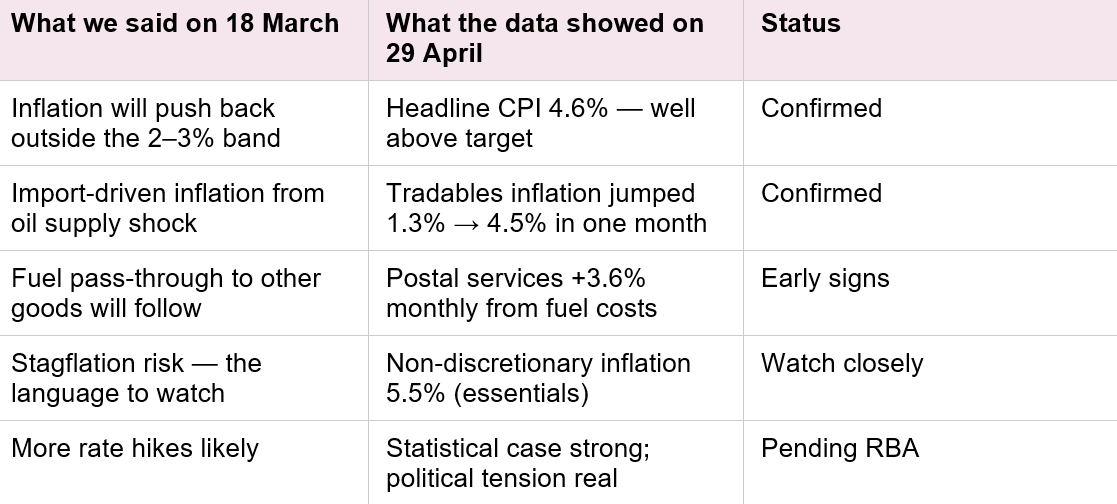

On 29 April, the Australian Bureau of Statistics released the monthly CPI for March 2026. Headline inflation rose to 4.6% over the year up sharply from 3.7% in February, and well outside the Reserve Bank's 2 - 3% target band. Trimmed mean inflation, the RBA's preferred underlying measure, was unchanged at 3.3%.

The transport group was the standout. Annual transport inflation moved from -0.2% in February to +8.9% in March, a 9.1 percentage-point swing in a single month. Within that, automotive fuel rose 32.8% in the month of March alone, the strongest monthly rise since the series began in 2017. Diesel, which feeds directly into freight costs, rose 41%.

Tradables inflation, the part of the basket exposed to international supply jumped from 1.3% to 4.5% in one month. This is exactly the import-driven inflation channel we described in the webinar at Payble two months earlier.

Revisiting what we said on 18 March

During the emergency webinar we made several specific calls. For transparency, here's how each has tracked against the data released six weeks later.

Why we believe the data is still 30 days behind

Here is the part that should concern every finance team and Australian ratepayer. The CPI release captures prices through the end of March. It does not yet reflect what happened to oil markets in April.

Crude Oil WTI peaked near US$115 per barrel in early April and is currently trading at US$101.68 - still well above the historical mean of around US$73 per barrel. The April fuel surge will land in the next CPI release in late May.

There is also a second-order effect that takes longer to surface. When diesel rises 41% in a single month, the cost of moving every product around Australia rises with it.

Postal services already showed a 3.6% monthly increase in March from fuel pass-through. Food, building materials, retail goods; anything that travels by road follows on a lag of weeks to months.

In other words, the inflation print we are reading today reflects an economy that has not yet fully absorbed the shock. We expect the April and May data to show further acceleration, with the trimmed mean - currently anchored at 3.3% beginning to drift upward as second-round effects take hold.

The rate decision: statistical case versus political reality

The RBA is now in a difficult position. The statistical case for a rate hike is strong:

- Headline CPI is 1.6 percentage points above the top of the target band.

- Tradables inflation has more than tripled in a single month.

- Non-discretionary inflation (the cost of essentials people cannot avoid) is running at 5.5%.

- Forward indicators (April crude prices, freight pass-through) point to further rises in coming releases.

The political case for a hold is also real. The headline spike is driven by an exogenous supply shock from Middle East conflict and monetary policy can never fix oil supply. The trimmed mean remaining anchored at 3.3% gives the RBA a defensible narrative to look through the volatility and offer households relief from further mortgage pressure.

Our view: a 25 basis-point increase is the most statistically likely outcome at the next meeting.

Context: A hold is the political wildcard - influenced mainly by a lack of desire to pressure the Aussie ratepayer. A 50 basis-point move at a single meeting is unlikely but cumulatively, two further hikes over the coming meetings becomes increasingly probable if the second-round inflation we are forecasting comes through in the April and May data.

The uncomfortable truth: if the RBA holds for political reasons now, the inflation embeds, and the eventual correction is sharper. A hold today likely means a larger move later not no move at all.

What this means for local government

The webinar message on 18 March was that councils needed to prepare ahead of inbound community pressure for rates relief, and that policy responses would need to be rapid and iterative. That message is more justified today than it was six weeks ago, not less.

- Hardship policy review: expect a measurable uptick in rates relief enquiries over the next 60 days. Position your hardship pathways before the volume hits, not during it.

- Flexible payment arrangements: the case for flexible, smaller-instalment payment options strengthens with every CPI release that exceeds the band. They keep cash in ratepayers' offset accounts and reduce arrears risk for councils.

- Cash flow modelling: stress-test rates collection scenarios assuming a further 25 - 50 basis points of cumulative tightening over the next two RBA meetings.

- Community communication: elected members and customer service teams are on the front line. A simple, factual update on what's driving prices (fuel, conflict, supply) helps reduce frustration and channel it into constructive engagement.

Staying ahead of the next release

The next monthly CPI lands in late May. It will be the first to capture April fuel prices in full. Based on what we are seeing in the futures market and at the bowser, we expect it to confirm the trajectory we have been describing since 18 March.

To stay across what comes next, follow Payble and Dailius Wilson on LinkedIn.

We called this on 18 March. The data on 29 April confirmed it. The next 30 days will tell us how much further it has to run.

Dailius Wilson

Sources: ABS Consumer Price Index, Australia, March 2026 (released 29 April 2026); Crude Oil WTI spot price (4 May 2026).